Loan Amount ₹1,000 to ₹20,000 — Instant Small-Ticket Loans

Not every financial need requires a large loan. Sometimes it’s a pending electricity bill, a small medical expense, a mobile recharge shortfall, or a gap between salary dates — and that’s exactly what a small-ticket loan between ₹1,000 and ₹20,000 is designed for. Yuva offers this as a fully digital, unsecured personal loan, so you can borrow only what you actually need instead of taking a larger loan and paying interest on an amount you didn’t require. Whether you need a ₹1,000 loan for utility bills, a ₹5,000 instant loan for emergency expenses, or a ₹20,000 personal loan for short-term financial needs, Yuva allows eligible applicants to borrow only the amount they require through a fully digital process.

These small loans go through the same regulated lending process as larger loans — income verification, digital KYC, and a structured repayment schedule — just scaled down in ticket size and tenure. This makes them a practical option for short-term, low-value expenses rather than long-term borrowing.

Understanding Small-Ticket Loans, First

A small-ticket loan is simply a personal loan with a lower principal amount — typically anywhere from ₹1,000 up to ₹20,000–15,000 in the Indian digital lending market. Regulators and lenders don’t treat these as a separate legal category; the same RBI digital lending guidelines, interest disclosure norms (like the Key Fact Statement), and credit bureau reporting requirements that apply to a ₹2 lakh loan also apply here.

What differs is purpose and risk assessment:

- Purpose: Small-ticket loans are generally used for short-term, immediate needs rather than large planned expenses

- Tenure: Usually shorter — a few weeks to a few months, rather than a year or more

- Assessment: Lenders often process these faster since the exposure per loan is lower, but income and repayment checks still apply

- Credit impact: Timely repayment of even a small loan is reported to credit bureaus like TransUnion CIBIL and can help build your credit profile — the amount doesn’t need to be large to count toward your repayment history

This makes a ₹1,000–₹20,000loan a reasonable entry point for first-time borrowers, or a quick bridge option for anyone who needs a small amount without over-borrowing.

Features & Benefits

Borrow only what you need

no obligation to take a larger loan than your actual requirement

Unsecured

no collateral or guarantor required

Fully digital process

apply, verify, and receive funds from your smartphone

Quick digital processing

smaller ticket sizes are typically processed and approved quickly

Short, manageable tenure

repay over weeks or a few months instead of committing long-term

Credit-building opportunity

consistent repayment on a small loan is reported to credit bureaus, same as any other loan

Over ₹4,000cr+ disbursed

01 million+ app downloads

1 Lakh+ happy customers

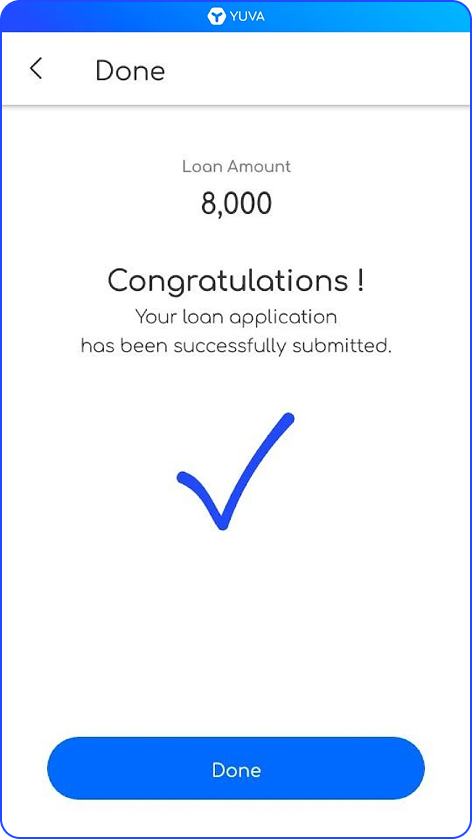

Steps to Apply

- Download the Yuva Personal Loan App

- Sign up and enter your basic details

- Upload the required documents

- Select your loan amount between ₹1,000 and ₹20,000, and your tenure

- Submit your application

- Wait for quick digital verification

- Get the amount credited directly to your bank account

Loan Configuration

Choose from flexible plans based on eligibility:

Instant Personal Loan

Amount: ₹10,000 – ₹1,00,000

Tenure: 3–9 months

Higher Personal Loan

Amount: ₹25,000 – ₹3,00,000

Tenure: 6–18 months

Salary Advance Loan

Amount: ₹10,000 – ₹50,000

Tenure: 1–3 months

Eligibility Criteria

The process is simple and inclusive.

Indian citizen

Age 21 years or older

Stable monthly income

Valid mobile number

Active bank account

Required Documents

Upload your documents online:

PAN Card

Aadhaar Card

Latest salary slip

Bank statement

Uses of These Loans

There are no restrictions for the borrowers.

Emergency medical expenses

Rent, bills, daily essentials

Car / two-wheeler repairs

Travel or family needs

Shopping or small purchases

Any urgent cash requirement

Yuva loan Interest Rate & Charges

Interest Rate : 2.75% – 3.5% per month*

Processing Fee : Up to 3%

Late Fee : 0.1% per day (after grace period)

Note: Interest rates, loan amount, and repayment tenure are determined after evaluating the applicant’s overall eligibility, including income, repayment capacity, employment stability, banking behavior, and credit profile where applicable.

Tips Before You Apply

- Borrow only the amount you actually need — a ₹20,000limit doesn’t mean you should take the full amount by default

- Check the total repayment amount (principal + interest + fees), not just the monthly EMI

- Keep your bank statements clean, with regular income credits

- Repay small loans on time — bureaus report these the same way as larger loans, so consistency matters more than size

- Avoid taking multiple small loans simultaneously to cover the same shortfall, as this can affect your credit utilisation and score

Smart Borrowing Tips

Small loan amounts can feel low-stakes, but they carry the same repayment obligation and credit-reporting consequences as any other loan.

- Only borrow what fits comfortably within your next pay cycle or repayment tenure

- Missing even a small EMI is recorded on your credit report and can affect future loan eligibility

- If you find yourself repeatedly taking small loans to cover recurring shortfalls, it may be worth reviewing your monthly budget or speaking to a financial advisor rather than relying on short-term credit

- Compare the total cost of borrowing against the actual expense you’re covering — for very small amounts, a flat processing fee can sometimes outweigh the benefit